Most hospitals in the United States operate as nonprofit entities,1 which exempts them from federal taxation in recognition of the benefits they provide to the community. This tax exemption represents a sizable amount, estimated at $24.6 billion in 2011.2 The size of the exemption has prompted debate about the favored tax status of these hospitals, as the amount and type of community benefit that they provide has been called into question.

Concerns about the justification for this large tax exemption prompted Congress to include community benefit requirements in the Patient Protection and Affordable Care Act (ACA)—requirements that most hospitals would have needed to comply with by 2013.3 These provisions require hospitals seeking tax-exempt status to conduct community health needs assessments (CHNAs) every three years and develop strategies to address those needs.4 According to the regulations governing these CHNAs, social determinants of health such as neighborhood safety, the availability of healthy foods, and whether residents earn a living wage should be considered as health needs and addressed in hospital strategies.5 These new regulations are meant to direct tax-exempt hospitals “to look beyond providing medical services to patients and to address the health needs of their communities.”6 The law does not, however, set any minimum value of benefits that must be provided in any category in order for hospitals to qualify for tax-exempt status.7

Although the ACA provides requirements for gaining tax-exempt status, the provisions it lays out may not guarantee that the community benefits provided by nonprofit hospitals actually address community needs. In 2014, hospitals nationwide spent an average of 8.1% of their total expenditures on community benefits, but community benefit spending varied considerably—from approximately 0.96% of total spending by hospitals in the lowest total spending decile, to 18.28% of total spending by those in the highest total spending decile.8 A similar study determined that the variation in community benefit spending did not correlate with measures of community need.9 Therefore, CHNAs and the implementation plans required by the ACA may not ensure that nonprofit hospitals provide sufficient and appropriate community benefits to justify their valuable tax-exempt status.

In addition to an apparent lack of correspondence to community needs, nonprofit hospitals’ community benefit spending often does not necessarily address broad community needs. Community benefit measures, as described by the U.S. Internal Revenue Service (IRS), can be split into two broad categories: expenditures directly related to patient care and those associated with community service. Expenditure categories that fall into the former category include charity care (subsidized care for patients who meet criteria set by the hospital), unreimbursed costs for means-tested government programs (split into Medicaid and non-Medicaid programs), and general subsidized health services (services provided at a financial loss). Community service categories include community health improvement services (i.e., childhood immunization efforts), research, health professions education, and contributions to community groups that carry out community benefit activities. A nationwide analysis of community benefit spending by nonprofit hospitals found that over 85% of community benefit expenditures went toward direct patient care.10 Although providing subsidized direct patient care is a valuable benefit, this skew limits the resources available for broader community health initiatives, such as preventative care or population health.

Hospitals in Harris County, Texas

We investigated whether the national trends described above held true for hospitals in Harris County, Texas. In 2016, 16.6% of Texans were uninsured, the highest rate in the country. The uninsured rate for Harris County has historically been 2–3 percentage points higher than that of the state of Texas.11 The additional financial burden of caring for these uninsured patients placed on Harris County hospitals makes this region of particular interest in examining hospitals’ community benefit spending. We also conducted a subanalysis of the Texas Medical Center (TMC), the largest medical complex in the world. The large teaching and research hospitals in the TMC have different resources and different spending pressures and goals than smaller, non-TMC hospitals. Although the TMC’s vision includes “becom[ing] the world leader in health and life sciences” and “ultimately transform[ing] human health,” it does not include any specific goals related to local community health benefits.12

Although benefiting the local community may not be a primary goal of TMC institutions, previous research has found a positive relationship between increased community benefit spending in community service categories and the teaching status of a hospital.13 As most of the institutions within the TMC have teaching status, we would expect them to have higher levels of spending on community service. Motivated by the significant distinctions between hospitals within the TMC and nonTMC hospitals, we conducted a comparative study between these two groups, including private for-profit and public institutions in addition to private nonprofits. We compared their overall levels of community benefit spending, as well as breakdowns by type of spending.

Methodology

Although previous related research has used data from the IRS Form 990 Schedule H—which hospitals use to report community benefits they provide each tax year—for this study, we collected data on hospital community benefit spending from the Texas Department of State Health Services (DSHS). Compared to accessible Form 990s, the data available from the DSHS encompassed more hospitals in Harris County and contained more recent expenditure information. For instance, the most recent Form 990 available for some hospitals was from fiscal year 2013 or 2009, whereas all data obtained from the DSHS pertained to fiscal year 2014.

Complete expenditure data were not available for several Harris County hospitals. Some hospitals did not have any community benefit spending data available; these were excluded completely from the analysis. Community benefit spending data were available for other hospitals, but data on their total expenditures were not; therefore, community benefit spending as a percentage of total expenditures could not be calculated, and they were excluded from the total community benefit expenditure comparison. They were, however, included in the spending breakdown analysis (see Appendix A for a breakdown of the hospitals evaluated in each analysis).

Because categories of community health spending reported to the Texas DSHS did not always correspond exactly to the categories defined by the IRS, we found equivalent or similar categories of spending within the DSHS data. The significant differences between the categories we used and the categories defined by the IRS were in the community health improvement and community benefit operations category—which in our analysis represents public health education efforts—and in the subsidized health services category, which in our analysis also includes preventative care initiatives.

Categories were constructed from the worksheets of the 2015 Annual Statement of Community Benefits Standard (ASCBS), which is distributed by the Texas DSHS. Questions from these worksheets were combined as necessary to construct categories analogous to those found on the IRS Form 990, Schedule H (see Appendix B for more details about how specific categories were determined). Community benefit expenditures as a percentage of total expenditures were calculated using total expenditure data from the 2015 ASCBS for each hospital.

Total Community Benefit Spending in Harris County

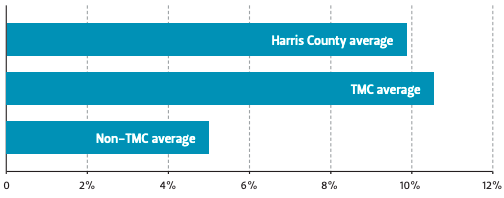

On average, Harris County hospitals that were included in this study spent 9.81% of total expenditures on community benefit provision, as seen in Figure 1. This figure is close to the 2014 national average of 8.1%.14

Figure 1 — Charitable Spending as a Percentage of Total Expenses

Similar to the results found by Young et al., individual institutions varied greatly in their specific community benefit spending, especially when comparing TMC and nonTMC institutions.15 Without accounting for total budget differences between TMC and non-TMC institutions, TMC hospitals averaged spending over six times as much on community benefit provision than non-TMC hospitals ($55.8M versus $8.7M, respectively). To account for the larger total budgets of TMC hospitals, we calculated the total community benefit expenditures of each included hospital as a percentage of the total expenditures.

Even after accounting for differences in total expenditures, TMC hospitals on average spent more than twice as much on community benefit provision as a percentage of total expenditure than nonTMC hospitals (Figure 1).

Spending Breakdowns of the TMC and Non-TMC Hospitals

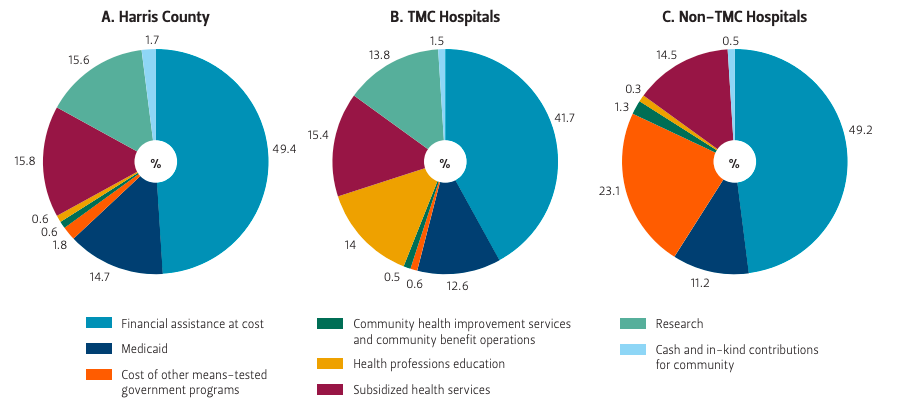

Similar to the findings of Young et al., most community benefit expenditures by both groups of hospitals went toward direct patient care (Figure 2A).16 Both groups spent just over 50% of total community benefit expenditures on charity care and the unreimbursed costs of means-tested government programs such as Medicaid (Figure 2B, 2C). Because TMC institutions spent over twice as much as non-TMC hospitals on total community benefit provision as a percentage of total expenditure, their total spending on charity care and the unreimbursed costs of means-tested government programs was also over twice that of non-TMC hospitals as a percentage of total expenditure.

Figure 2 — Spending Breakdown by Categories

Source Authors’ own analysis.

Larger differences in spending patterns appeared when examining how the rest of community benefit expenditures for both groups is allocated (Figure 2B, 2C). TMC institutions devoted 27.8% of total community benefit spending to research and health professions education, while non-TMC hospitals devoted less than 1% to these areas. Non-TMC institutions instead spent 23.1% of their total community benefit expenditures on other means-tested government services, while TMC hospitals spent less than 1% on them. Both groups spent less than 2% of total community benefit expenditures on community health improvement services and community benefit operations.

Discussion

It is difficult to compare spending categories in this analysis with the categories of direct patient care and community service used in previous literature due to the differences in definitions of the subsidized health services and the community health improvement categories. Our analysis also included for-profit and public hospitals in addition to nonprofit institutions. However, some conclusions can still be drawn. For instance, given that most TMC institutions have teaching status, it appears that this status does correlate with increased total community benefit spending, similar to previous results (see Figure 1).17

Although TMC hospitals spend more on community benefit provision than non-TMC hospitals, over 80% of that community benefit spending goes toward charity care, unreimbursed costs of means-tested government programs, health professions education, and research. Although these expenditures do provide a benefit and correspond to the TMC’s mission to “serve the health, education and research needs of Texas and the world,”18 they leave little room for spending on community health improvement and subsidized health services, which would likely provide more direct benefit to the local community. Another possible explanation for TMC institutions’ spending being skewed toward these categories is that they serve a large uninsured population. These hospitals spend 41.7% on average of total community benefit expenditure on charity care, while the national average is just over 25%.19 The large uninsured population in Harris County may be limiting the ability of TMC institutions to spend on community health improvement or subsidized health services. The ACA and the resulting decrease in uninsured rates was expected to reduce the demand for charity care and allow community benefit dollars to instead be shifted to other initiatives, such as those related community health.20 But Texas’s decision not to expand Medicaid and recent national policy decisions diminishing the efficacy of the health insurance marketplaces could minimize this spending shift.

The ACA’s requirement that nonprofit hospitals conduct CHNAs every three years was designed to encourage hospitals to increase spending on community health initiatives.21 A study reviewing Texas CHNAs that were available in early 2014 found wide variation in terms of the approach to and quality of the reports.22 We viewed a small selection of more recent Harris County TMC and non-TMC hospital CHNAs and found similar results. The CHNAs are similar in terms of the data they provide on Houston area demographics and health statistics, resulting in a large overlap in reporting between hospitals. But the implementation plans vary greatly. For example, Memorial Hermann Health System’s implementation plan includes a breakdown of specific objectives to reach the goals they have set based on three priority areas. Each objective details specific baseline and target measures, such as the number of educational programs or presentations (e.g., an outreach program for elementary students highlighting bicycle helmet safety, mental health education sessions for nurses and physicians) and the number of patients receiving appropriate screening (e.g., emergency room patients screened for Hepatitis C and HIV).23 While some hospitals such as Memorial Hermann provide detailed plans and/or dollar amounts to be spent on programs, others provide only vague goals. Providing a common template or specific guidelines for CHNAs could increase the value to both hospitals and the community of conducting the assessments and increase accountability in addressing the needs identified.

The goals of the ACA include an increased focus on preventative care and population health, but currently, much of the community benefit spending undertaken by Harris County hospitals focuses on financial assistance to patients. Even with regard to the CHNAs, hospitals tend to focus on access to care over community health initiatives. One strategy to address the disparity between the purported goals and reality involves making it easier for hospitals to have certain categories of community-building activities recognized as community health improvement spending. Under current IRS rules, community benefit spending covers spending on community health improvement, which includes “activities or programs…carried out or supported for the express purpose of improving community health.”24 As explained by Rosenbaum et al., the IRS defines “community building” to include more general community improvements such as physical, environmental, and economic development (e.g., efforts to develop safe, affordable housing or advance student achievement). Since these activities fall outside of the IRS’s definition of a community benefit, they must meet additional criteria and be justified separately to the IRS as items that support community health in order for hospitals to credit such activities toward their community benefit expenditures.25 Making it easier for hospitals to do so may incentivize them to engage in more of these activities and allocate more of their community health expenditures toward endeavors that benefit communities more broadly. Combining this strategy with clearly defined minimum requirements for certain categories, such as subsidized health services or community health improvement, could further increase the breadth of the impact of a hospital’s community benefit expenditures.26 These strategies can better justify the tax exemption enjoyed by these institutions and help align their actions with the needs of their communities.

Endnotes

1. Julia James, “Health Policy Brief: Nonprofit Hospitals’ Community Benefit Requirements,” Health Affairs, February 2016.

2. Sara Rosenbaum, David A. Kindig, Jie Bao, Maureen K. Byrnes, and Colin O’Laughlin, “The Value Of The Nonprofit Hospital Tax Exemption Was $24.6 Billion In 2011,” Health Affairs 34, no. 7 (July 2015): 10, http://doi.org/10.1377/hlthaff.2014.1424.

3. Gary J. Young, Chia-Hung Chou, Jeffrey Alexander, Shoou-Yih Daniel Lee, and Eli Raver, “Provision of Community Benefits by Tax-Exempt U.S. Hospitals,” New England Journal of Medicine 368, no. 16 (April 2013): 1519–27, http://doi.org/10.1056/NEJMsa1210239.

4. Ibid.

5. Mary Crossley, “Health and Taxes: Hospitals, Community Health and the IRS,” Yale Journal of Health Policy, Law, and Ethics 16, no. 1 (August 2016).

6. Ibid.

7. James, “Health Policy Brief.”

8. Gary J. Young, Stephen Flaherty, E. David Zepeda, Simone Rauscher Singh, and Geri Rosen Cramer, “Community Benefit Spending By Tax-Exempt Hospitals Changed Little After ACA,” Health Affairs 37, no. 1 (2018): 121–24, http://doi.org/10.1377/hlthaff.2017.1028.

9. Young et al., “Provision of Community Benefits.”

10. Ibid.

11. U.S. Census Bureau, “Small Area Health Insurance Estimates—Interactive Data and Mapping,” accessed January 22, 2018, https://www.census.gov/data-tools/demo/sahie/sahie.htmls_appName=sahie&menu=grid_proxy&s_statefips=48&s_ stcou=48201&s_year=2015,2014,2013,2012,2011,2010.

12. Texas Medical Center, “Our Vision,” accessed January 31, 2018, http://www.tmc.edu/about-tmc/vision/.

13. Young et al., “Provision of Community Benefits”; Young et al., “Community Benefit Spending.”

14. Young et al., “Community Benefit Spending.”

15. Young et al., “Provision of Community Benefits.”

16. Young et al., “Community Benefit Spending.”

17. Young et al., “Provision of Community Benefits”; Young et al., “Community Benefit Spending.”

18. Texas Medical Center, “Our Vision.”

19. Young et al., “Provision of Community Benefits.”

20. Young et al., “Community Benefit Spending.”

21. Ibid.

22. Cara L. Pennel, Kenneth R. McLeroy, James N. Burdine, and David Matarrita-Cascante, “Nonprofit Hospitals’ Approach to Community Health Needs Assessment,” American Journal of Public Health 105, no. 3 (March 9, 2015): e103-13, http://doi.org/10.2105/AJPH.2014.302286.

23. Memorial Hermann Health System, “Memorial Hermann Texas Medical Center Community Benefits Strategic Implementation Plan 2016,” http://www.memorialhermann.org/uploadedFiles/_Library/Memorial_Hermann/MHHS% 20SIP%20TMC%20FINAL%20Sept%202016.pdf.

24. Internal Revenue Service, “2016 Instructions for Schedule H (Form 990).”

25. Sara Rosenbaum and Bechara Choucair, “Expanding The Meaning Of Community Health Improvement Under Tax-Exempt Hospital Policy,” Health Affairs, January 2016.

26. Daniel B. Rubin, Simone R. Singh, and Gary J. Young, “Tax-Exempt Hospitals and Community Benefit: New Directions in Policy and Practice,” Annual Review of Public Health 36, no. 1 (March 18, 2015): 545–57, http://doi.org/10.1146/annurevpublhealth-031914-122357.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.